HARTALEGA HOLDINGS BERHAD

Business Summary

Hartalega Holdings Berhad (Hartalega Bhd) is a listed glove manufacturing company. Hartalega Bhd is a global supplier of nitrile and rubber gloves, although having all of its manufacturing facilities in Malaysia. Started off in 1988 as a single line operation, Hartalega Bhd now has an annual capacity of 36 billion pieces as of 2019.

Their state-of-the-art manufacturing complex is dubbed the National Gloves Complex (NGC). Launched in the year 2014, it was a massive initiative to bring Hartalega Bhd’s annual production volume from 14 billion pieces of production up to 44.6 billion pieces by the year 2020. It aims to transform the glove manufacturing industry, once perceived as low-tech and foreign labour intensive to a high-tech and innovation-driven operation.

Hartalega Bhd’s main business is in the manufacturing of gloves, namely nitrile gloves and rubber gloves. Both gloves have a dozen of specifications which are well suited for each industry’s requirement, be in industrial, healthcare, laboratory or the food and beverage sectors.

Last update: 20.11.2019

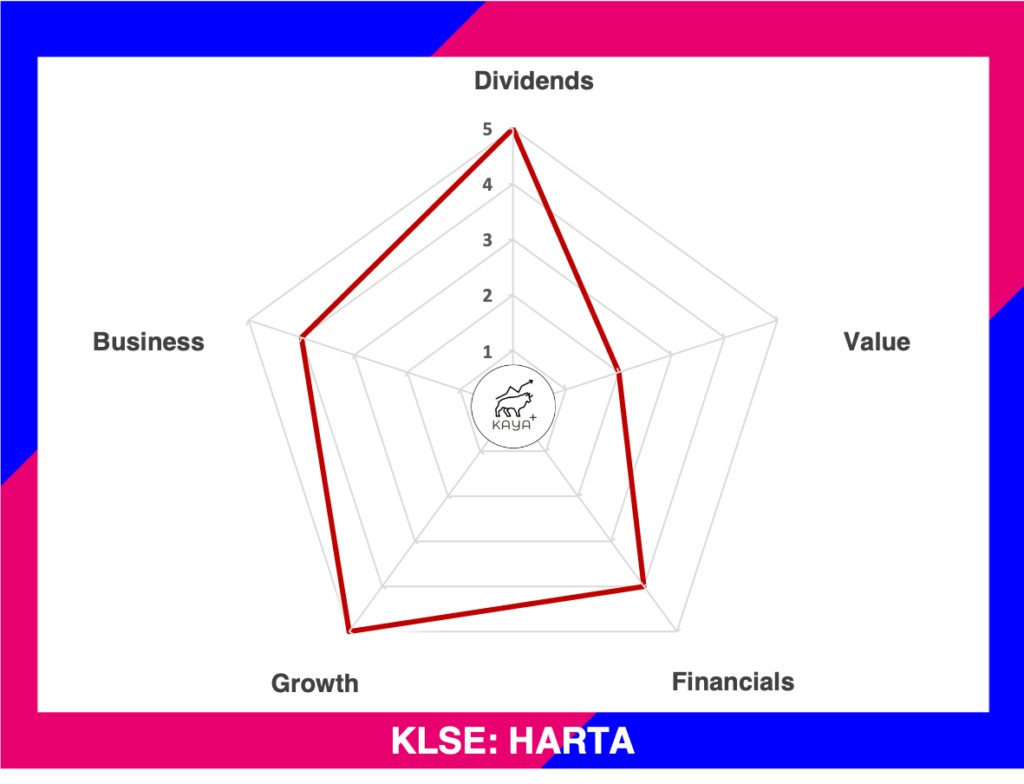

Dividends (5/5): ⭐ ⭐ ⭐ ⭐ ⭐

Value (2/5): ⭐ ⭐

Financials (4/5): ⭐ ⭐ ⭐ ⭐

Growth (5/5): ⭐ ⭐ ⭐ ⭐ ⭐

Business (4/5): ⭐ ⭐ ⭐ ⭐

Reference: (i) MyKayaPlus Metrics Definition (ii) MyKayaPlus Metric Evaluation Scale

Management

Hartalega Bhd was originally formed as Hartalega Sdn Bhd by Mr Kuan Kam Hon, who currently now serves as the Executive Chairman of Hartalega Bhd. His sons Mr Kuan Mun Leong serves as the Managing Director of Hartalega Bhd and Mr Kuan Mun Keng serves as Director of Business Development and Corporate Finance.

The Kuan family collectively holds around 50% of the ownership of Hartalega Bhd, via direct and indirect interests. As of 2019, the total remuneration package of the total Hartalega board of directors stands at around RM 2 million per annum, which is 0.1% of their annual revenue.

Financial Performance

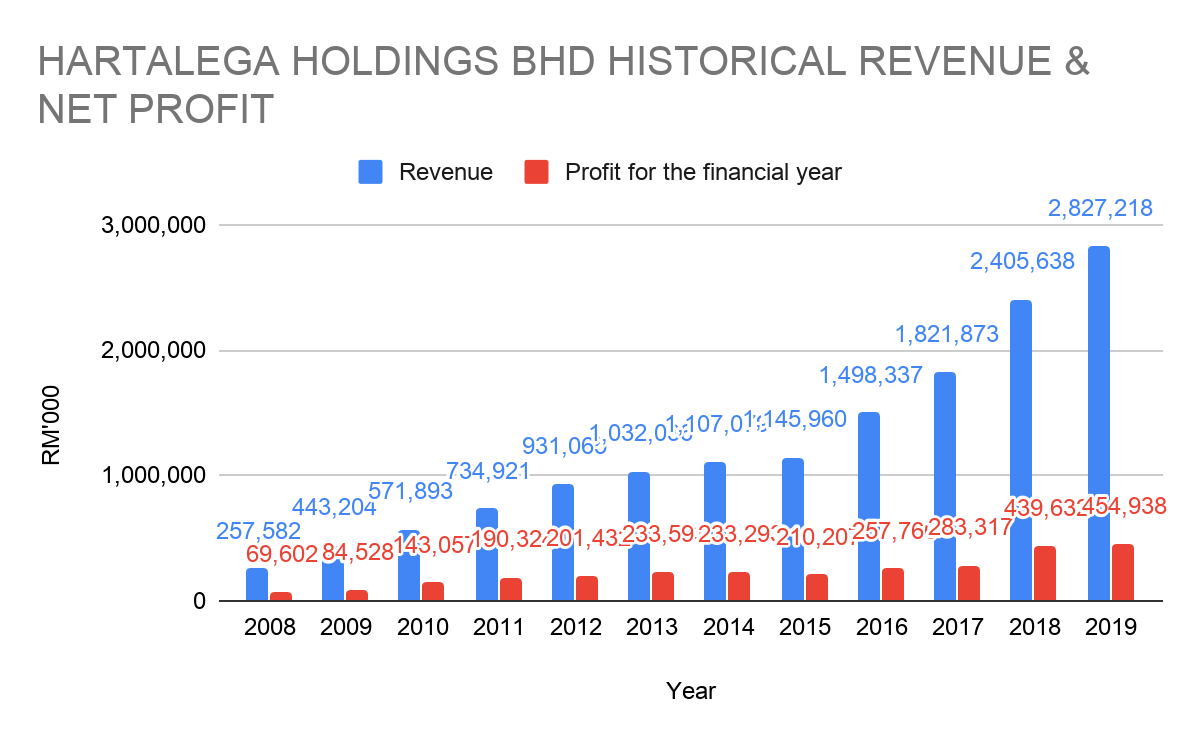

Hartalega Bhd has seen explosive growth over the last 10 years. The growth particularly exploded after the year 2014, which coincides with the period the NGC started production. Net profit also saw growth from RM 70 million to RM 455 million as of the year 2019. Hartalega Bhd was one of the first movers that disrupted the rubber gloves market by offering nitrile gloves. Nitrile gloves are stronger than traditional latex gloves, while also offering higher chemical resistance.

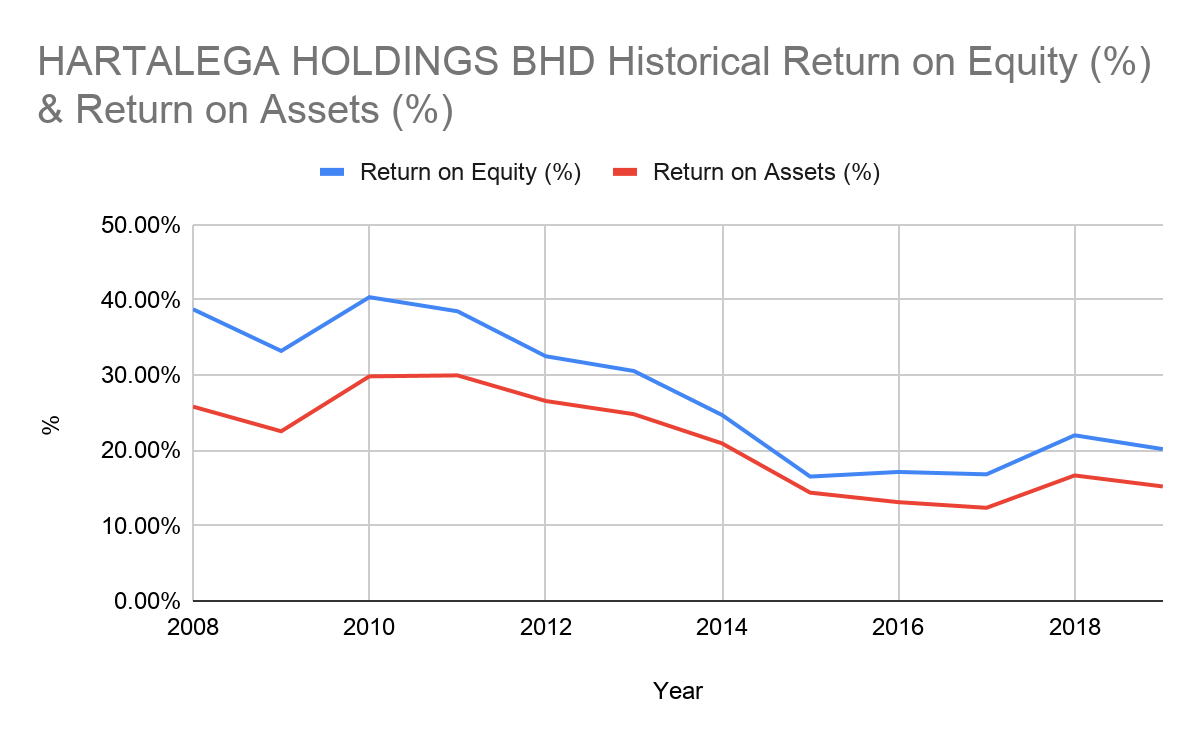

Hartalega Bhd has among the best Return on Equity (ROE) and Return on Assets ROA) among all glove-making companies. As of 2019, it has an ROE of 20+% and a ROA of around 15%. Even though profit has increased a lot in the last 10 years, ROE and ROA are on a downtrend as the number of equity increases more than the profits generated. This is because of Hartalega Bhd has a low gearing ratio, where the majority of its funds required for expansion is obtained via equity financing. Nonetheless, it still clocks a respectable ROE and ROA when compared with other glove companies.

Balance Sheet

| Year | Assets (RM’000) | Liabilities (RM’000) | Equities (RM’000) | Current Ratio |

| 2019 | 2,992,095 | 732,865 | 2,259,230 | 2.18 |

| 2018 | 2,631,979 | 634,588 | 1,997,391 | 2.09 |

| 2017 | 2,286,774 | 601,988 | 1,684,786 | 1.91 |

| 2016 | 1,961,100 | 457,074 | 1,504,025 | 2.83 |

| 2015 | 1,457,452 | 186,791 | 1,270,661 | 3.06 |

In the year 2019, Hartalega Bhd has Assets of around RM 3 billion, liabilities of RM733 million and Equities of RM 2.2 billion. The current ratio is strong at 2.18, which gives us assurance Hartalega has enough current assets to meet its current liabilities.

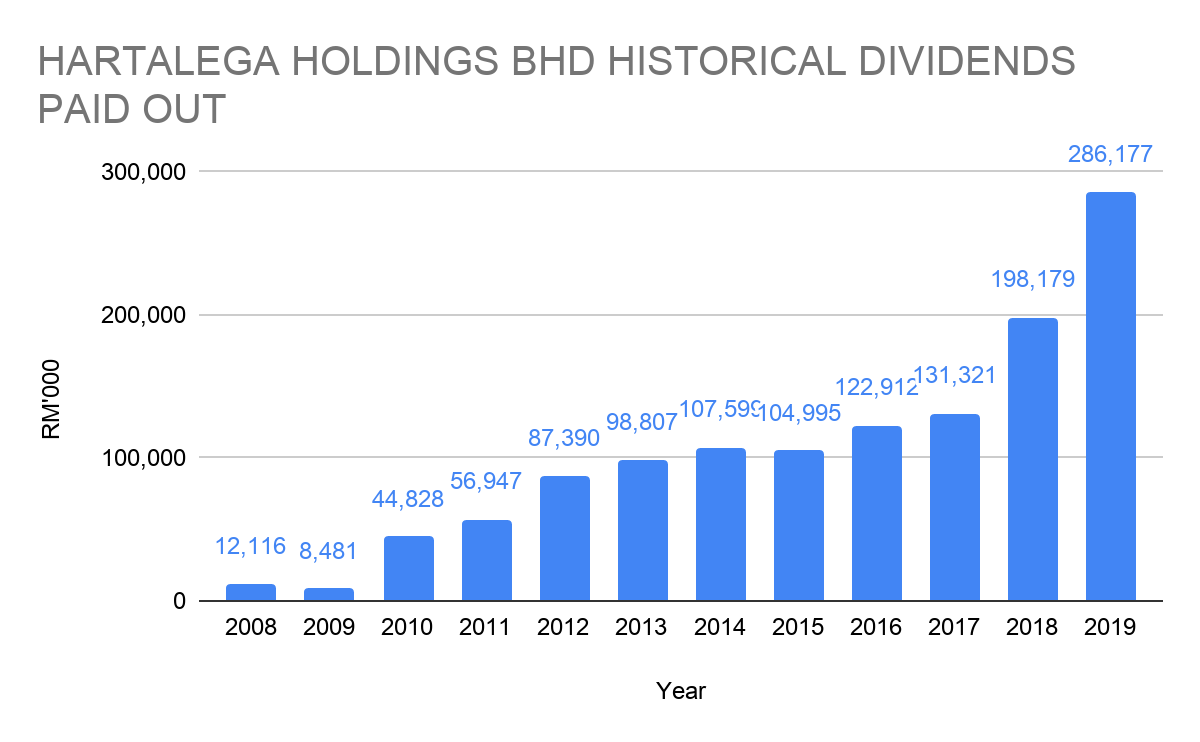

Free Cash Flow & Dividends Paid Out

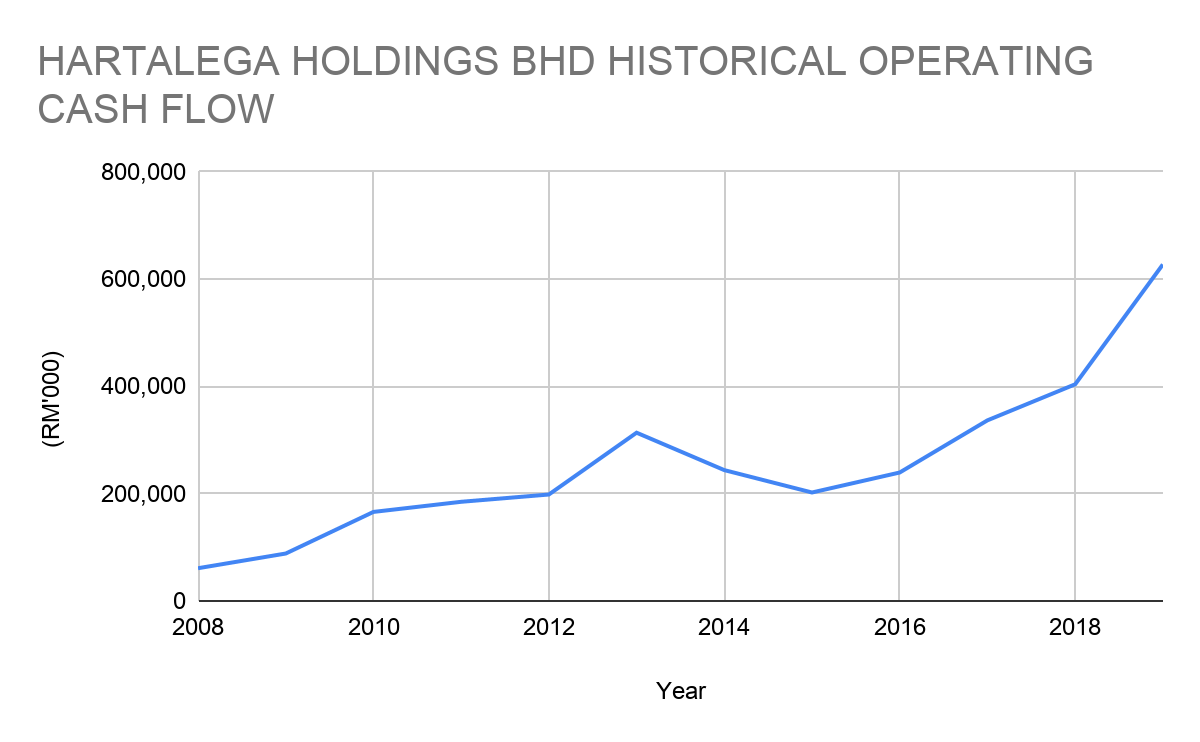

Source: HARTALEGA BHD ANNUAL REPORT

Glove manufacturing is a cash cow business. Hartalega Bhd has proven that with the expansion of its NGC, and an increase in revenues and profits, operating cash flow also trends up accordingly. Dividends paid has a 10 compounded average growth rate of around 20.4%!

The misconception about finding a dividend stock is that it has to have good dividend yield. But all math experts would know that dividend yield is just a mathematical formula that divides the dividends per share by the current share price to obtain a TRAILING indicative dividend yield.

Should the share price is inflated, you will get a low dividend yield, and if the share price is cheap, you will get a high dividend yield. Hartalega Bhd is actually a fantastic dividend-paying company as it’s glove manufacturing business is a cash cow business. Plus it also has a dividend policy of distributing a minimum of 45% of its annual profits to shareholders as dividends

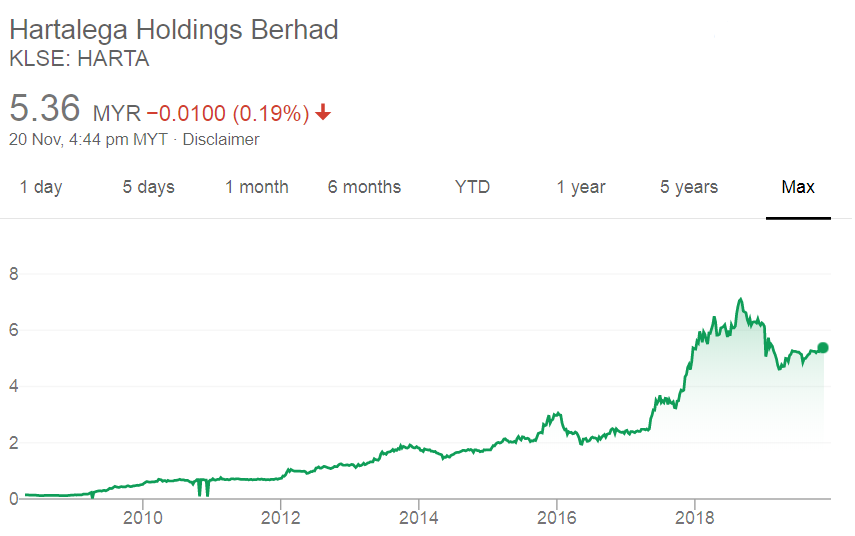

Of course, since Hartalega is trading at a Price to Earnings ratio of roughly 40 times, many investors would automatically disregard Hartalega as a good dividend stock, as its current trailing dividend yield is at 1.54% per annum.

Price

MyKayaPlus Verdict

A share price always tags along with a company’s prospects and profits. Hartalega Bhd is actually a combination of growth and dividend company. Not only has it shown explosive growth but its dividend payout has also increased in tandem.

Hence, it is not surprising that such a wonderful company is currently trading at a Price to Earnings ratio at about 40 times. Of course, it is a high price to pay even for such a fantastic company.

But it all boils down on how Hartalega will continue to grow as it maps out its expansion plans beyond 2020. The NGC was a grand plan to raise its capacity to 44 billion pieces of gloves per annum capacity. Now as we approach the year 2020, investors will be curious about what would be the next 10-year plan to justify its currently hefty price tag.

If you would have bought Hartalega Bhd in 2008 since its IPO using RM 100, you would be now sitting on an astounding paper gain of roughly RM 35,000, excluding dividends? This is the power of value investing, a return that no traders could comfortably beat!

Do you see Hartalega Bhd firing on all cylinders in the next coming 10 years? Let us know in the comments below!

Like our Hartalega Holdings Bhd analysis? Please check out their competitor – Top Glove Bhd’s analysis here