8 Things You Should Know About AirAsia Bhd’s 2019 3rd Quarter Report

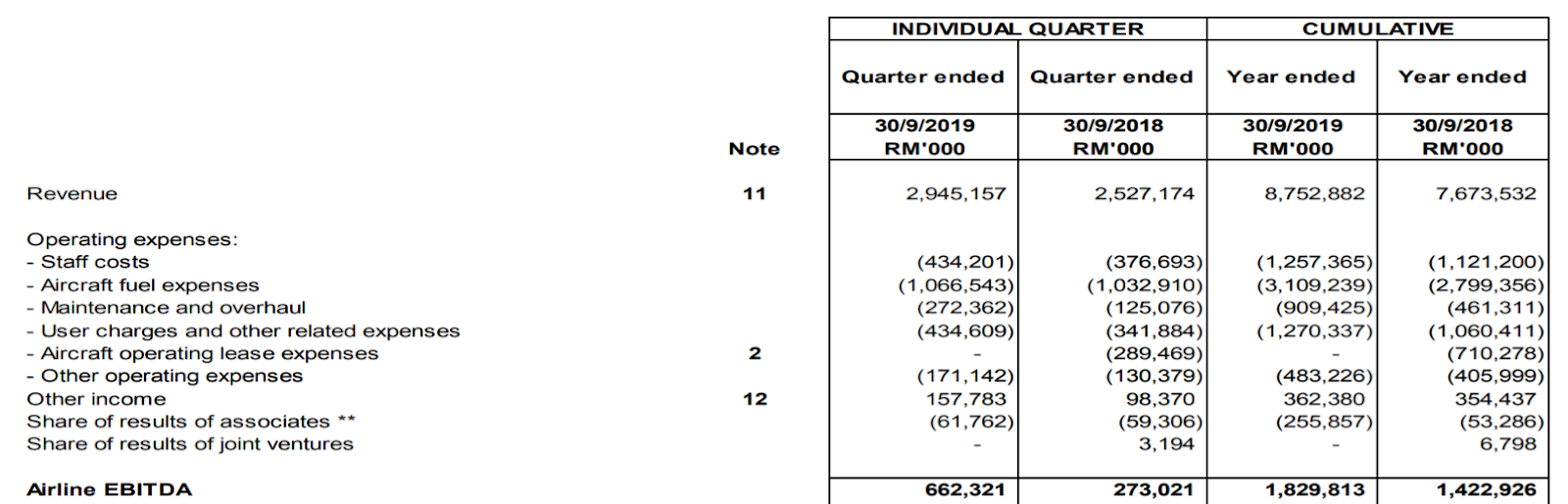

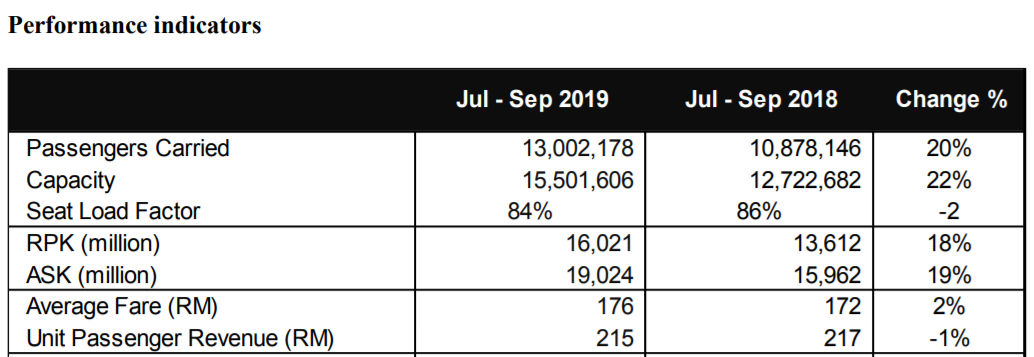

1. Spectacular Quarter-on-Quarter Revenue Growth

Revenue increased from RM 2.5 billion to RM 2.9 billion which is an 18% gain. The average fare, however, is flat at RM 176 compared to RM 172 quarter-on-quarter, giving a suggestion that revenue increased is due to increased of passengers carried, which increased 20% quarter-on-quarter from 11 million to 13 million.

Verdict: Fantastic!

2. Majority of operating expenses marginally increased

Staff Costs increased roughly RM 50 million quarter-on-quarter while fuel costs also increased from RM 1.03 billion to RM 1.066 billion, both of which are a fairly small increase. But ratio wise, the expenses are very much in control, since airlines related earnings before interest, tax, depreciation and amortization (EBITDA) quarter-on-quarter increase of roughly RM 400 million is more or less directly from the revenue increase.

Verdict: Good!

3. Non-Arline EBITDA of operating expenses increased

Teleport, AirAsia Group Bhd’s logistics arm and business service, increased by RM 18 million. But Airasia.com, Bigpay Group and Red Beat Ventures Group are suffered heavier loses. In total non-airline EBIDTA decreased RM 10 million.

Verdict: Losing money or earning lesser is always a negative thing. But a quick check that all of these new business ventures have shown promising triple-digit revenue growth. So based on this we would put this as a promising factor.

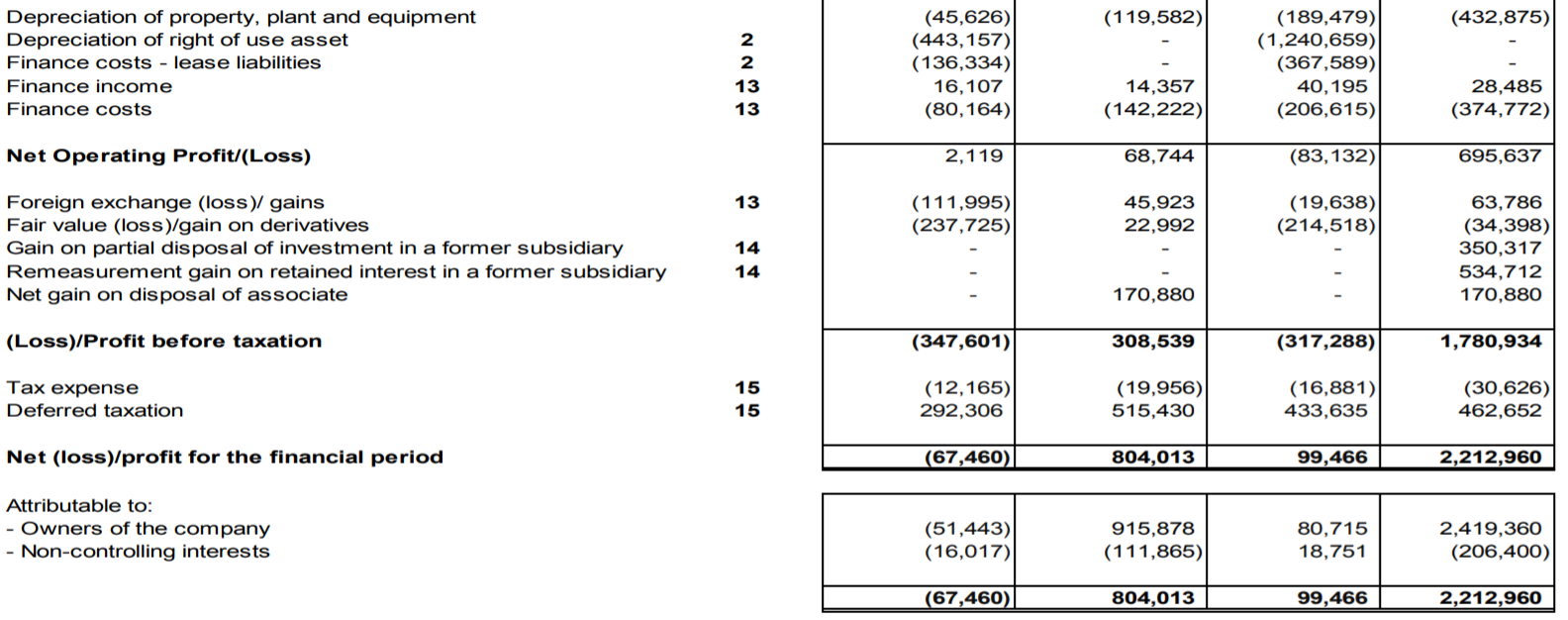

4. The Elephant in the room – Depreciation and Forex Losses

First of all, due to the adoption of MFRS 16: Leases, which replaces MFRS 117, AirAsia Bhd is required to acknowledge the depreciation expenses of Right-Of-Use assets (leased aircraft which they happily sold away and distributed special dividends).

Since the adoption started early this year, we can see a RM 443 million worth of ROU assets for the current quarter and a cumulative of RM 1.24 billion depreciation costs. Ouch!

And just as you thought that was the only bummer, Foreign exchange losses were at RM 111 million, hand in hand with its fair value loss on derivatives at -RM 238 million.

Verdict: Of course the quarter report is bad. But it was majorly a change in financial and accounting standards that actually exacerbated the loss. Still, a loss is a loss, and for this, we would have to agree that AirAsia Bhd failed to deliver its profits.

5. Current ratio is a little tight

One of the nitty-gritty stuff we also look at is how confident AirAsia Bhd is able to manage its near term commitments with the amount of cash and projected cash received. There is a small shortfall of RM 1 billion-plus between the highlighted current liabilities and current assets.

Why we purposely focus on them is that these numbers are more liquid and more cash related, which we deem more representative of AirAsia Bhd’s cash flow management.

Verdict: This is a bit of a concern, but believe that loans and borrowings can be drawdown to pay off any upcoming commitments

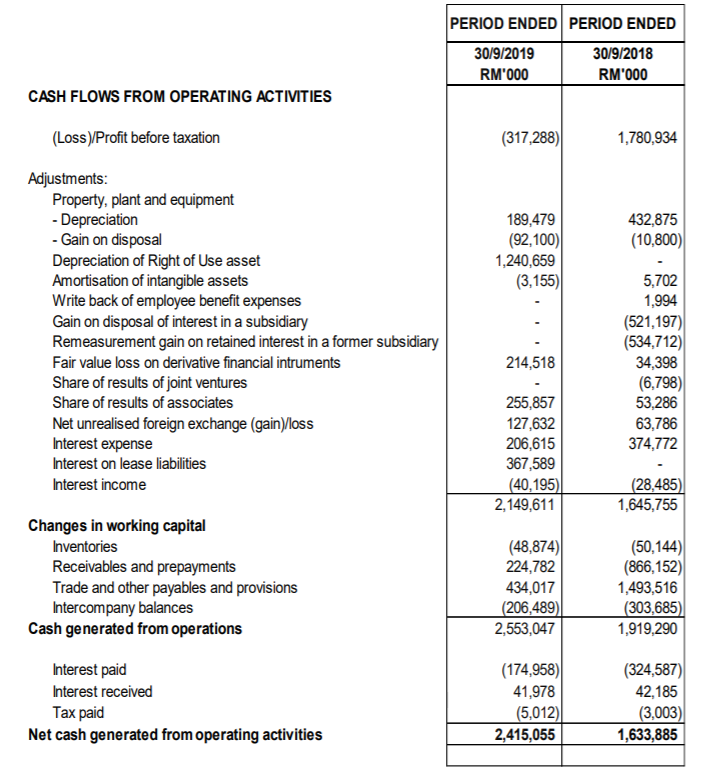

6. Cash Flow From Operating Activities

Once we put adjusted back all the non-cash expenses, we noticed that at least there was an increase in net cash generated from operating activities. Running an airline is a very asset-heavy business, and it is no real surprise that Airasia Bhd’s profit and loss suffered under the new MFRS.

But we would really need to keep an eye on its current liabilities as mentioned beforehand as a near term concern.

Verdict: We give Airasia a plus point for generating more cash from their key operating businesses. But the amount of cash generated will be proportionate to their sales volume and margins. So in order for this to sustain or even increase, both sales volume and margin has to grow. Which means more expensive tickets!

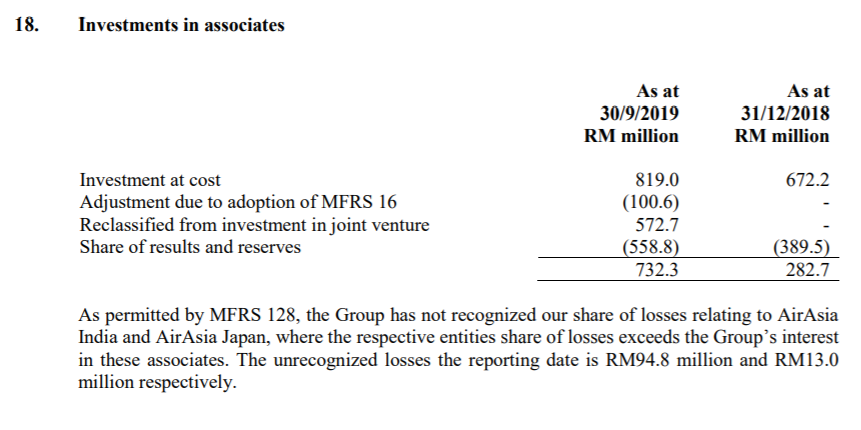

7. Losses at AirAsia India and AirAsia Japan are not recognised!

Verdict: In essence, both operations in India and Japan are still bleeding money. But hey since both are still experiencing growth so we give AirAsia the benefit of doubt on the prospects of both countries. Remain neutral

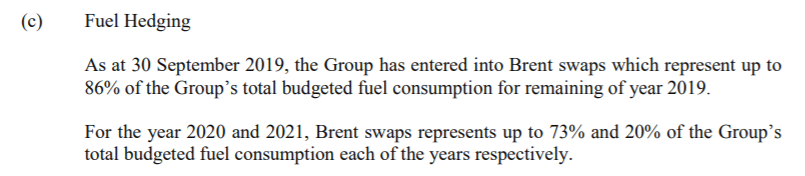

8. A large chunk of its fuel is hedged

Verdict: It is surprising that a huge chunk (73%) of its 2020 budgeted requirement is hedged. Of course, no one ever knows where the prices of Brent are heading towards. But historically, current Brent prices seem to be on the rise and on a 10-year comparison, price is fair and in the middle

Conclusion

Yes, it is a red quarterly report for AirAsia Bhd this time round. Looks like Tan Sri Tony Fernandes would have to eat his words. But if we dig deeper into its quarterly report, at least we still see the company growing rapidly at all fronts.

I also noticed that Teleport for social enterprise is also live already. So big credits and kudos to AirAsia Bhd on growing its business into multiple segments, but still managing to synchronise them via the Big member system. Time will only tell when AirAsia Bhd will shake off its tag as an airline company to be recognised as a conglomerate.

Check out our latest AirAsia Group Berhad stock analysis here.

Also, check out our AAX analysis here to see if there are any same problems faced by both airlines