Malayan Banking Bhd. V.S. DBS Group Holdings Ltd.

Malaysia and Singapore are two different countries sharing yet very similar pasts. Both countries used to be strategic port bases for the British during their occupation. In fact, both countries have been together more than they are apart. Before Singapore was even colonized by the British it was nominally under the Johor Sultanate. Mathematically speaking, Singapore and Malaysia have been together for close to 400 years, and only 60+ years separated.

But one similar point that both countries share is that both have grown leaps and bounds ever since independence. Of course, both countries fought for independence from the British government, and then Singapore left Malaysia. Both countries have then started to become the few clusters of South-East Asian countries experiencing high growth and potential.

Banking is one of the sectors that play a huge role in developing both Malaysia and Singapore. In fact, both dominant banks from each respective countries have grown in tandem with their domestic economic growth rate. The massive growth pivoted banks from Malaysia and Singapore to take up the top 5 spots of South East Asia largest banks by market capitalization.

Are you curious how Malaysia’s biggest bank, Malayan Banking Berhad would stack up against Singapore’s biggest bank, DBS Group Holdings Limited? If you are, then let’s do a head-to-head comparison!

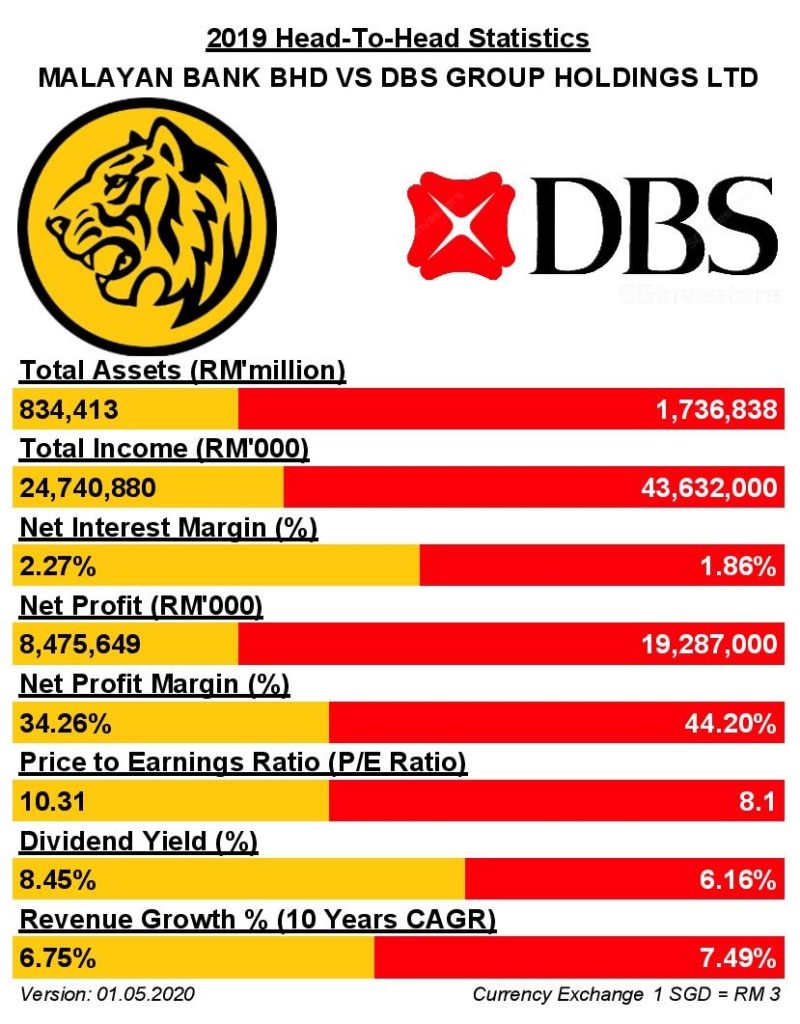

1. Total Assets

Assets play a huge role in evaluating a bank’s worth since most of a bank’s assets consist of cash. Since both banks operate in different countries, let’s convert DBS Bank’s figures from Singapore Dollar (SGD) to Malaysian Ringgit (MYR). The conversion factor used will be 1 SGD = RM 3. Looking at the total assets, DBS bank is more than twice the size of Maybank Bhd. DBS bank’s total asset for the fiscal year of 2019 stands at SGD 579 billion. Maybank Bhd’s total assets stood at RM 834 billion.

2. Total Income & Net Interest Margin

Banks derive a huge chunk of their income via interests from loans. For the fiscal year 2019, DBS Bank registered a total income of SGD 14.5 billion. Maybank Bhd’s total income was RM 24.7 billion. Compared under the same currency, DBS registered 57% more total income versus Maybank Bhd.

Next, we move on to compare the Net Interest Margin (NIM). Maybank Bhd actually pips DBS Bank in this segment. Maybank’s NIM was 2.27% while DBS Bank’s NIM stood at 1.86%. This means that Maybank Bhd is actually earning more interest returns compared to DBS bank. In terms of total income in terms of quantity, DBS actually beats Maybank nice and clean.

3. Net Profit and Net Profit Margin

Revenue is just the total amount of sales done. What investors value most is the net profit. DBS bank not only registered a higher total income but also a higher net profit. Net profit for FY 2019 is at SGD 6.4 billion. Maybank Bhd, on the other hand, manages to rake in a net profit of RM 8.5 billion.

Net profit margin wise, DBS bank registered a whopping 44% versus Maybank Bhd’s 34%. That means DBS Bank is actually more profitable in retaining its profits versus Maybank Bhd.

4. Price to Earnings Ratio and Dividend Yield

Next, we compare the valuations of both banks using the Price to Earnings Ratio and Dividend Yield. As of writing, Maybank is trading at a P/E of 10x while DBS bank is having a P/E of 8x. On a side-by-side comparison, it does seem that DBS bank is trading at a discount, even though having higher profit margins.

In terms of dividend yield wise, Maybank again registered a far more favourable trailing yield of 8.45%. DBS is 2% lesser at 6.16%.

How is DBS Bank earning more profits yet having a lower dividend yield?

The answers lie at the Dividend Payout Ratio!

For FY2019, Maybank Bhd paid out 87.8% of its earnings as cash dividends, indicating a dividend payout ratio of 87.8%. DBS bank, on the other hand, had a dividend paid out ratio of 50%.

The higher dividend payout ratio but muted global economical outlook gave Maybank Bhd a higher dividend yield!

5. Growth

Although both banks are considered large caps in their respective markets, they are still registering growth year-on-year.

Based on the latest historical 10 years, DBS bank registered a Compounded Annual Growth Rate of 7.49%. Maybank is a bit slightly behind at 6.75%. On averagely, both banks manage to grow their total income by 6-7% every year for the past 10 years.

Banking is an age-old yet evergreen business segment. And usually, banks tend to grow bigger and stronger as time goes by, with prudent management.

Moreover, situated in a high growth potential segment of Asia, both banks are at the right place to grow together. Of course, the recent COVID-19 definitely slammed the brakes on the growth trajectory of South East Asia. But according to CSIS, South East Asia would see a strong rebound in the year 2021.

MyKayaPlus Verdict

Side by side comparison wise, DBS Bank definitely trounces Maybank Bhd with their impressive numbers. But then again, both banks operate in different countries and have different focuses in their growth strategies. It is possible to still bet on the long term bright South-East Asian economies by keeping a close eye at both banks.

Both banks are key examples to their peers in prudent management and strong growths. Banks being banks, they would definitely grow if enough time and patience are given to them.

Perhaps that is why Warren Buffett’s portfolio is so heavily skewed towards the financial sector!

What do you think? Which bank do you like out of both? Or are both already in your stock portfolio? Let us know in the comments section below!