IGB REIT V.S. SUNWAY REIT

Malaysians love the shopping mall.

It doesn’t have to be a special occasion for big reputable malls to be jam-packed.

The idea of going to the malls at the peak hour (between 12 pm to 8 pm) gave me shudders. The snaking queues of cars entering the parking lots plus the long unbearable waiting. Not to even mention the illegal one-way direction we sometimes drive against. All for the sake of catching hold of parking lot left vacant within seconds.

Fortunately, for shopping mall REIT investors, these scenarios should be able to make you smile. It means business is good. And when business is good, so will the distribution paid out to REIT investors. As a REIT investor, knowing that business is good in the malls I invested in increases my patience while looking for parking.

Two of the more well-known REITs that have a track record in generating increasing returns are IGB REIT and Sunway REIT.

So which REIT is the better one? Or are both equally good? Let’s do a head-to-head comparison!

1. Total Assets & Number of Properties

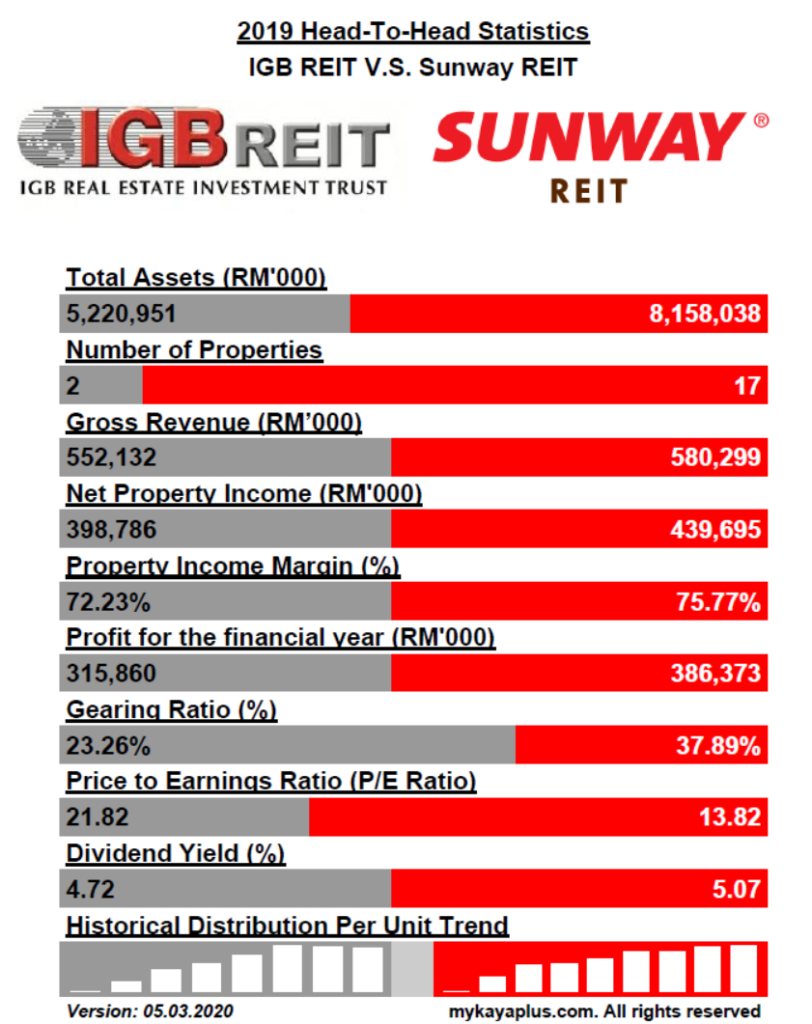

IGB REIT has only 2 units of investment properties, namely the Mid Valley Megamall and The Gardens Mall ever since IPO in the year 2012. Its total assets have been relatively stable, save for some revaluation gains along the years. On the other hand, Sunway REIT boasts a portfolio of 17 investment properties with a total asset size of RM 8 billion.

Sunway REIT has been on acquisition mode ever since its IPO, growing from 10 properties with a total property value of RM 4.4 billion to RM 8 billion in the span of 9 years.

Verdict: Sunway REIT takes it home for its aggressive growth model.

2. Gross Revenue

The number of investment properties will be useless if it does not generate rental income. The next criteria we look at the gross revenue that both REITs are earning.

Even though with just 2 units of investment properties, IGB REIT’s gross revenue is actually quite close to Sunway REIT. IGB REIT registered gross revenue of RM 552 million in the year of 2019. Sunway REIT on the other hand generated around RM 580 million for the year 2019.

Why do 15 more investment properties generate just a little more than additional of RM 30 million of revenue?

By looking at the breakdown, Sunway Pyramid Shopping Mall generates more than 50% of Sunway REIT’s gross revenue. Revenue contributed by Sunway Pyramid Shopping Mall alone is more than the remaining 16 properties all put together!

This is a unique situation where IGB REIT shows that less can be more. By just focusing solely on retail malls, IGB REIT consistently grew its revenue. Compared to Sunway REIT, some of the properties are not able to generate high rental like Sunway Pyramid Shopping Mall.

Verdict: IGB REIT edges out Sunway REIT in terms of quality properties even though with lesser property units.

3. Net Property Income & Property Income Margin

Does how much gross revenue a REIT earns translate to the same net income? Are the REIT managers managing the expenses of a REIT well?

The next criteria we take a look at the net property income and the margin of both IGB REIT and Sunway REIT.

IGB REIT brought in RM 399 million of net property income for the fiscal year of 2019. This translates to a property income margin of 72%. Sunway REIT registered a net property income of RM 440 million, which is a property income margin of 76%.

Verdict: Sunway REIT edges out IGB REIT for margin and net profit for the fiscal year of 2019.

3. Gearing Ratio

Contrary to what people think that REITs are safe, they can run into trouble if their debt is not well managed. Next, we look at the gearing ratio of both IGB REIT and Sunway REIT.

Gearing ratio measures the percentage of assets funded by borrowings. IGB REIT recorded a gearing ratio of 23% while Sunway REIT had a gearing ratio of 38% as of the fiscal year 2019.

Both REITs have a gearing ratio lower than 50%, which is the max limit set by the regulations. A lower gearing ratio means that REITs can borrow up to the max level of 50% to fund acquisitions.

Verdict: IGB REIT is the more passive REIT when it comes to acquisition. So it has a lower gearing ratio compared to Sunway REIT.

4. Valuation and Yield

There are a few methods to evaluate a REIT. Usually, all of them are used together to form a more holistic justification.

IGB REIT’s last trading price showed a trailing Price to Earnings ratio of 22 times, while Sunway REIT is at a P/E of 14 times. Based on the P/E ratio, Sunway REIT is cheaper than IGB REIT

IGB REIT’s latest trailing gross dividend yield is at 4.72%, which is lesser than Sunway REIT’s 5.07%. A unit invested in Sunway REIT will yield a higher distribution yield return.

Price to book value wise, IGB REIT is trading at close to 1.8 times while Sunway REIT is just at 1.2 times. It means should you were to buy IGB REIT, you are buying a fraction of Mid Valley Megamall and The Gardens Mall at 1.8 times more than the valuation price. Based on Price to book value, Sunway REIT is still cheaper

Verdict: Sunway REIT trounces IGB REIT in valuation and yield.

MyKayaPlus Verdict

Why is IGB REIT so much more expensive compared to Sunway REIT even though with just two properties?

The Malaysia property market is indeed fascinating in its own ways. Retail REITs are traded at a premium due to its reliable and predictable business model.

IGB REIT is purely in the retail REIT segment with two very good shopping malls. The quality of the properties in its asset allows it to bring in more foot traffic. This is why the property valuation of its asset can continue to go higher.

And a more valuable property can command a higher rental income from its tenants.

Sunway REIT also has its crown jewel which is the Sunway Pyramid Shopping Mall exhibiting similar trends like the Mid Valley Shopping Mall. Property value continues to appreciate consistently along the years with higher rental income as well.

No doubt Sunway REIT still puts in the effort to grow its portfolio by doing acquisitions. But so far all the acquisitions are not from the retail side, hence contributing a lesser increase in rental income.

Contrary to most people think, REIT investing is an asset play. Only great assets can command great rental. And great rental will be translated to higher distributions. Higher distributions will then drive the unit price higher.

Hence, IGB REIT exhibits a more solid investment. The only weakness of IGB REIT is its more passive approach. Should Sunway REIT continues to grow consistently, it would out-earn IGB REIT with more quality properties in the future. So both REITs have their own strengths and are good at their very own unique ways since Distribution Per Unit has been always on a steady rise

So do you think there are other REITs which can outclass IGB REIT or Sunway REIT? Let us know in the comments section below.

DISCLAIMER

The information available in this article/report/analysis is for sharing and education purposes only. This is neither a recommendation to purchase or sell any of the shares, securities or other instruments mentioned; nor can it be treated as professional advice to buy, sell or take a position in any shares, securities or other instruments. If you need specific investment advice, please consult the relevant professional investment advice and/or for study or research only.

No warranty is made with respect to the accuracy, adequacy, reliability, suitability, applicability, or completeness of the information contained. The author disclaims any reward or responsibility for any gains or losses arising from direct and indirect use & application of any contents of the article/report/written material