5 Things To Know Before Investing In Ping An Insurance

Ping An Insurance (HKG: 2318; SHA: 601318) might be unfamiliar to most of us. But it is one of the largest insurance companies in China and also the world.

For those who are aware of Ping An, its valuation as of the time of writing might have piqued your interest. But then again, it is crucial to go through some vital points prior to assuming value has arisen for Ping An.

Here are 5 things you need to know about Ping An before you invest.

1. Ping An is a full-fledged financial conglomerate

Ping An Insurance started off in 1988 as a property and casualty insurance company. Over the years, it has grown and diversified into insurance, banking, asset management, financial services, and healthcare services.

In 2009, Ping An became a strategic investor in Shenzhen Development Bank, which rebranded into Ping An Bank in 2012.

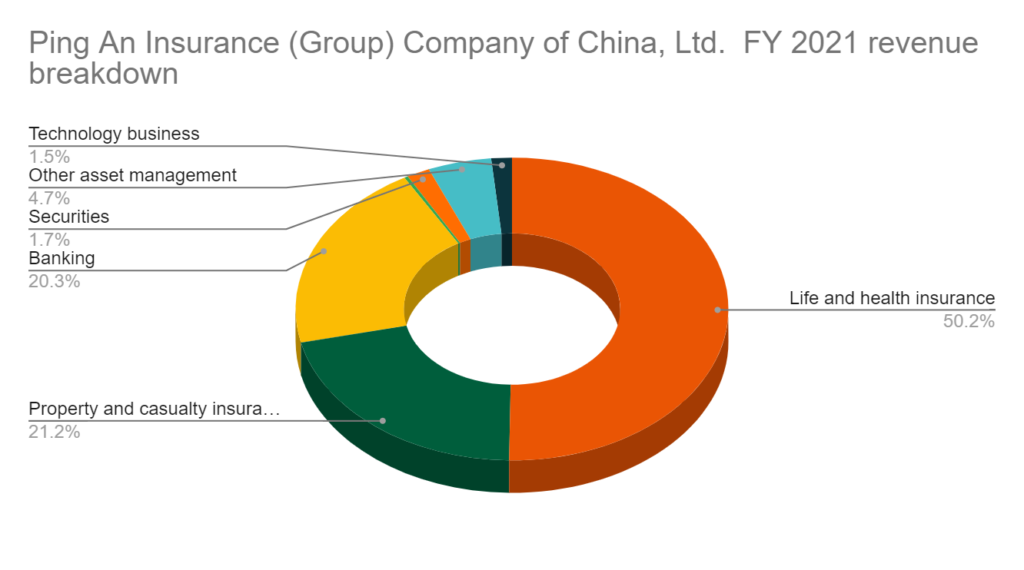

As of today, insurance contributes to around 70% of its total revenue. Banking constitutes 20%, while the rest is by its securities and asset management system.

Not many financial institutions have a strong insurance and banking pillar. Ping An is definitely one of them.

2. It is not a traditional boomer stock

The banking and insurance business is archaic. But it remains as relevant as of today, as they form in an integral part of mankind’s capitalism.

While easily more than half of the financial institutions around the world remain traditional as of today, Ping An has clearly set itself apart from its peers.

Ping An started its technology pillar and has quickly doubled down on its initiatives. It counts Lufax Holding, OneConnect, and Autohome as its new technology initiatives that complement its current bread-and-butter business.

Lufax Holding is a technology-empowered personal financial services platform. It utilizes AI-enabled and data-driven approaches in SME credit facilitation. It also offers middle-class and affluent investors wealth management solutions through its similar approach. The technological approach would then help suggest products and services that Ping An Insurance can offer, be it insurance or wealth planning.

OneConnect, a technology-as-a-service provider for financial institutions, helps banks and insurance companies undergo digitalization transformation. Its technology empowers banks to digitalize from marketing, wealth management, and services while helping insurance companies to manage contracts, claims, services, and settlements.

Autohome is a company that helps enhance the car-buying and ownership experience for auto consumers in China. From user-generated content on a wide array of cars to make the purchase decision and the entire ownership cycle, Autohome became the go-to website for people in China to purchase cars. It also provides other value-added services, including auto financing, auto insurance, used car transactions, and aftermarket services.

As you can see, the technology business serves as a digital enabler to help Ping An’s core businesses, which revolve around insurance and banking.

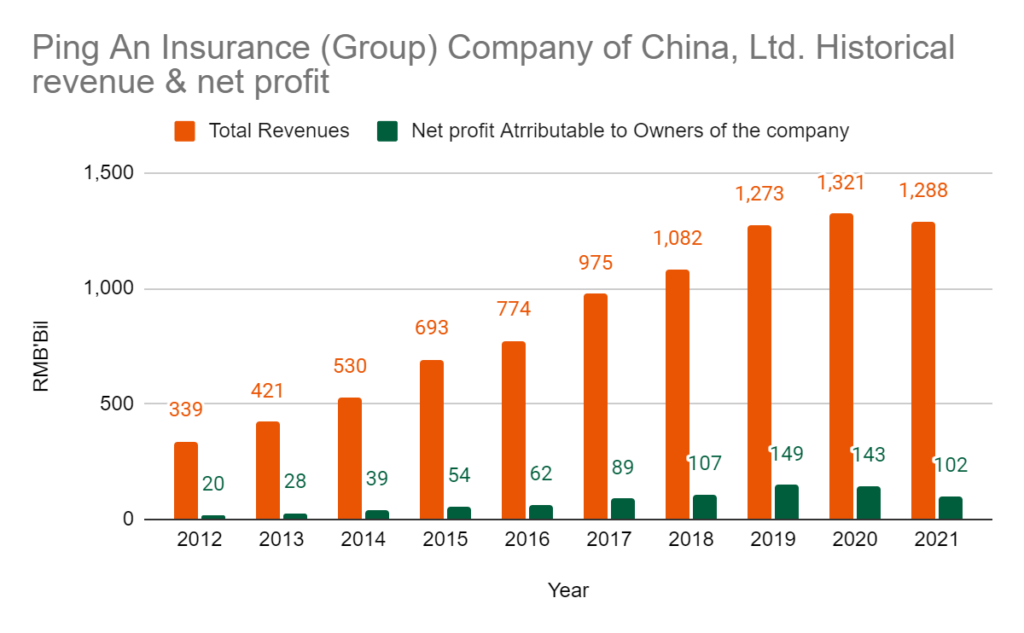

3. Revenue and profit have been growing except for FY 2021

Ping An Insurance has shown tremendous growth over the past 10 years. Revenue grew by 16% CAGR for the last 9 years, while profit was up close to 20% CAGR for the same tenure.

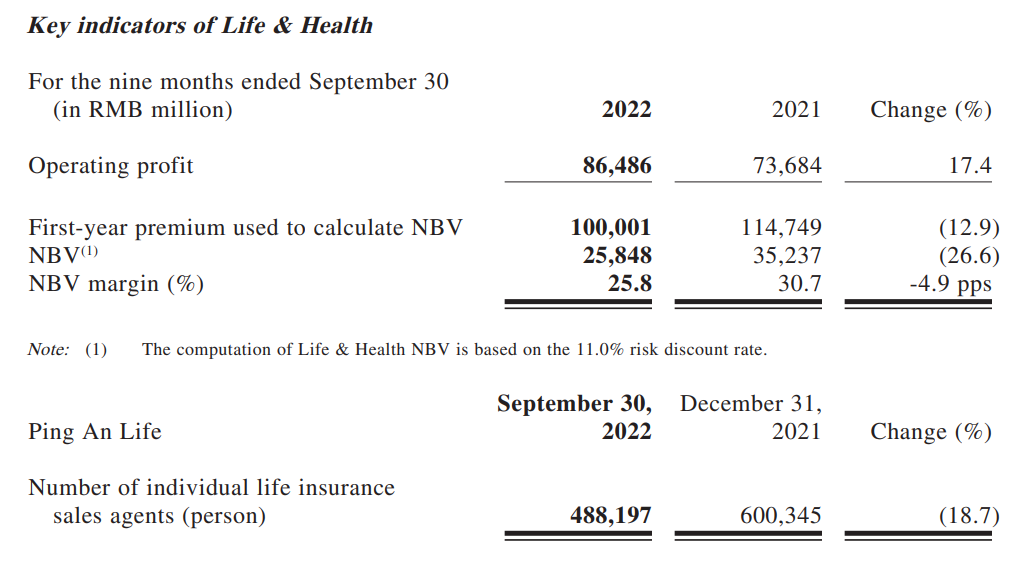

YoY-wise, the total revenue growth momentum came to a halt. Ping An underwent a transformation and reorganization of its life and health insurance agent force. New business value (“NBV”) of Life & Health

dropped 23.6% year on year to RMB 37,898 million in 2021.

Coming into the latest 9M’22 results, Ping AN’s NBV for life and health continues to experience a drop due to domestic sporadic COVID-19 outbreaks. However, operating profit was higher due to a leaner sales agent force.

4. Ongoing COVID-19 is affecting its Property and Casualty insurance operating profit

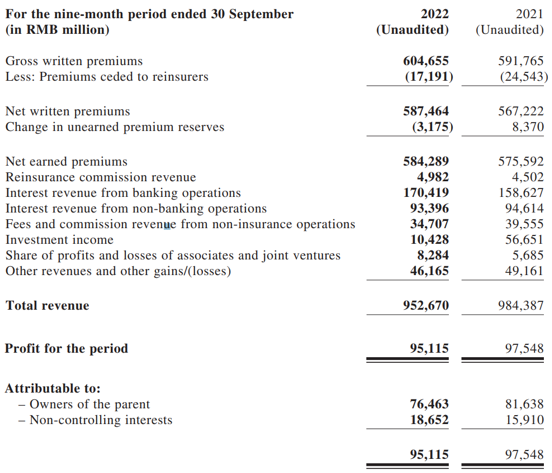

Although total revenue saw a revival for the 9M’22 versus 9M’21, total profit attributable to shareholders dropped.

The main culprit stems down to the lower operating profit from its property and casualty business. Although Ping An P&C’s premium income increased 11.4% year on year to RMB 222,024 million in the first nine months of 2022, the overall combined ratio rose by 0.6 pps year on year to 97.9% due to the rising claims of the guarantee insurance business amid the COVID-19 pandemic.

This led to its final profit attributable to shareholders of RMB 76.5 million, RMB 5.18 million lesser YoY.

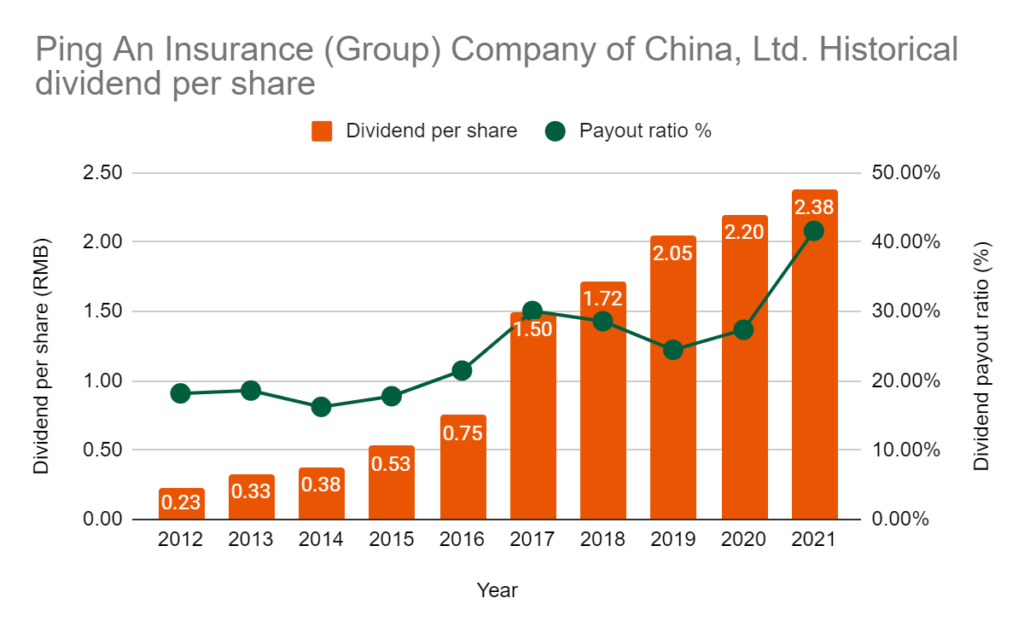

5. Increasing dividends for the last 10 years

Even though Ping An’s recent business has been disrupted by COVID-19 and some reorganization of its agent force, the dividends paid out were not affected at all.

Dividends per share have been increasing YoY for the past 10 years. Even though of the lower revenue and profit in FY 2021, the dividend per share increased due to a higher payout ratio.

Although the payout ratio is crucial in assessing the sustainability of a company’s dividend payout, Ping An’s latest payout ratio is around 40%, which does not raise any alarm bells.

MyKayaPlus Verdict

So is Ping An Insurance a clear buy? It has good fundamentals and pays out a strong stream of predictable dividends. It is also under book value as of now.

However, investors might be spooked by the Hang Seng Index correction and selldown. Ping An might remain a deep-value stock for a considerable amount of time.

Luckily at Kaya Plus, we have a proven methodology and blueprint to help us make decisions on whether we should acquire shares like Ping An right now.

Think about it. a complete set of fool-proof rules that help qualify and eliminate companies for long-term holding, be it capital gains or dividend income.

And we call it the Dividend Gems, where we empower like-minded people to learn how to find and analyze dividend companies for their own!

Interested to know whether Ping An Insurance can be invested? Join us now and unfold the answers!