The 4% + 1% Return Yield Per Annum

The Relationship between Risk & Reward

Investment return yield and risk always go hand in hand.

Oddly so, I found a fun fact. Any form of growing your wealth without any risk, the word that we always use is “SAVINGS” (be it your savings account or current account)

In Malaysia, the highest risk-free rate return would be in the region of 4% per annum (p.a., as of the time of writing and subject to changes). Any Tom, Dick or Harry (or Ali, Muthu or Ah Hock in our case) is perfectly capable of achieving this return by just putting our money in the fixed deposit of a bank of your choice.

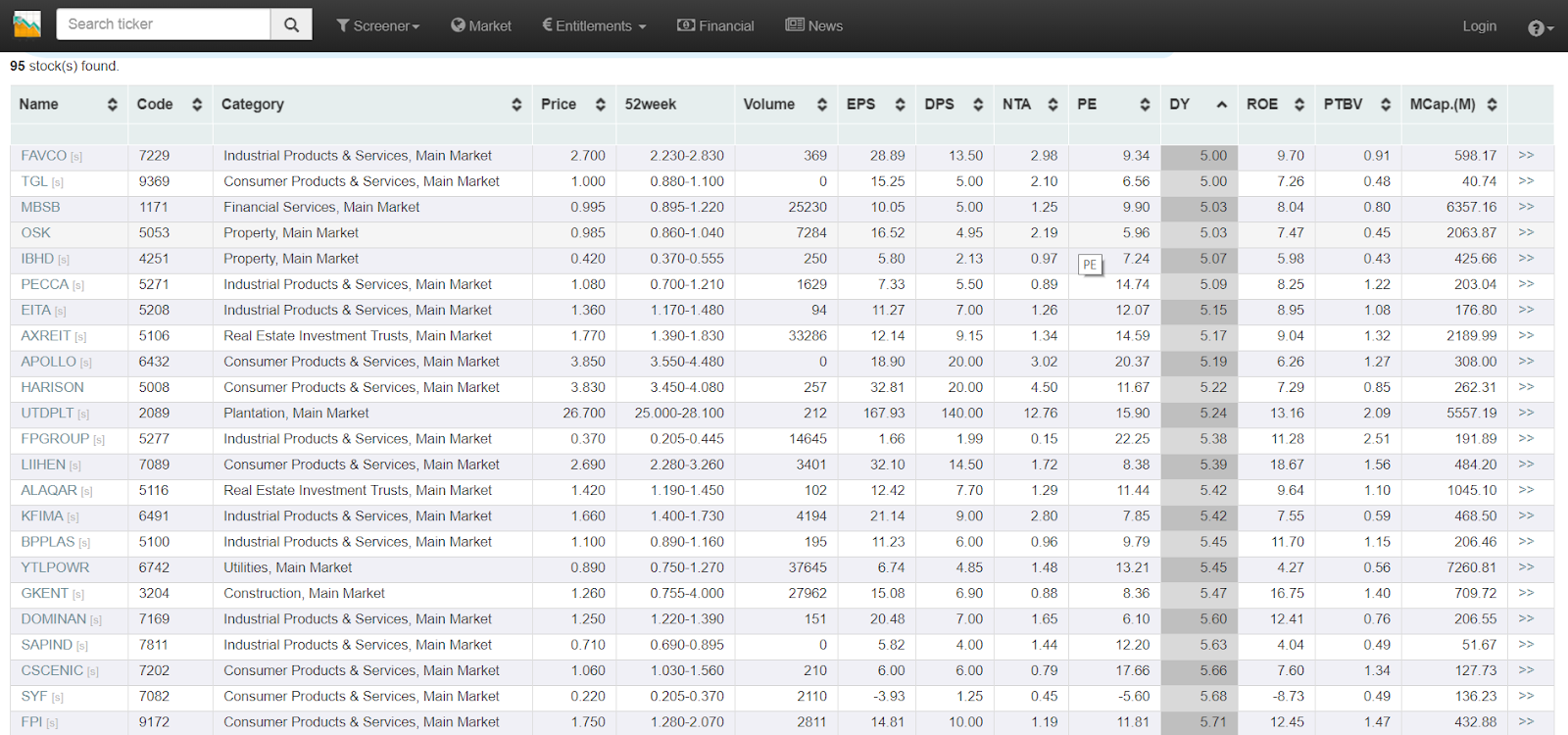

The real challenge starts when you look for 5% returns p.a. But honestly speaking, 5% returns p.a. investment opportunity is quite common in the stock markets. Do a simple screen your stock screener for a company that provides a 5% dividend yield are aplenty.

(In fact, I found 95 of them. Screened on the 1st of May 2019. Disclaimer: This is not a buy suggestion and purely for educational and illustration purposes)

Income Investing = Picking The Highest Yield?

So what do you do? Pick the highest yield and go full speed ahead?

Those who have some experience in investing know that things are never that straight forward. And I bet some of you have experienced dwindling dividends after buying a stock, or suffering a paper loss that even the dividend gains are unable to cover the capital loss.

It is by finding this additional + 1% more yield than the risk-free rate of 4% that you hit a major wall. You may ultimately end up getting a lesser gain or even a loss.

The risk of aiming that extra + 1% on top of a risk-free rate of 4% p.a. could lead you off track your journey to financial freedom.

Tip: Find out why high yield in investing is dangerous!

Know what is RISK. And it differs from everyone else.

So what is the RISK?

Risk is the PROBABILITY one has that allows a LOSING situation of a specific SEVERITY to happen. I purposely put that 3 words in CAPITAL letters, as they are the key essence that dictates what risk is all about.

PROBABILITY is the available options or outcomes in a given scenario. Put simply, you are allowing luck and fate to dictate your outcome (nothing different from gambling)

LOSING is the end results that happen if luck is not on your side.

SEVERITY dictates how much you stand to lose from an unfortunate situation. Losing RM1 is low risk and RM10,000 is high risk (relatively).

So how do we invest successfully and grow our wealth while containing risk? The 3 keywords that define RISK – Probability, Losing and Severity must be overcome and reduced!

How To Decrease Risk and Increase Reward?

We can reduce the probability and severity of losing by reading up, investing time to increase our knowledge and skill. By knowing what is needed to before you make a decision, you generally do better. Why do you go for driving class and obtaining a license? Because they serve as basic training and preparation before you start driving on the real traffic condition

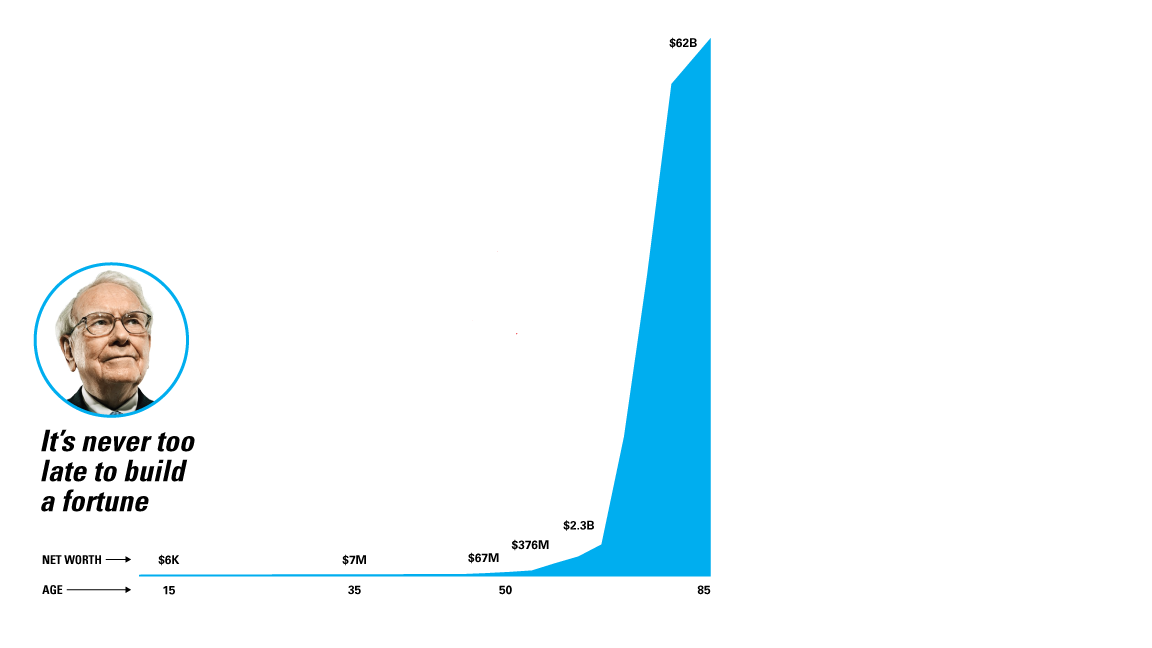

They say the first step is always the hardest. Same goes to the first +1% on top of the 4% risk-free rate. Behind every successful +1% return that all adds up are sacrifices, lessons. But you know what is the best part? That 4% +1% will keep compounding year on year. You’ll see. It gets easier and easier.

Proof? Warren Buffett was 30 years old when his net worth hit USD$ 1 million. Then he hit the USD$ 1 billion hurdle at the age of 56. To put in perspective, the first USD$ 1 million took 30 years to make. In the subsequent 26 years, he made 1000x of USD$ 1 million.

So what will you do to kick start your first 4% + 1%?

Which stock screener did you use?

Hi Katrina,

I think using KLSE Screener via computer.

Thanks,

Joo Parn