KOSSAN RUBBER INDUSTRIES BERHAD

Business Summary

Kossan Rubber Industries Berhad (Kossan Bhd) is a listed technical rubber product manufacturing company. Established in 1979, one of its key products manufactured are nitrile and rubber gloves and is often regarded as the third largest glove manufacturer in Malaysia, with manufacturing facilities in Malaysia and China. Kossan Bhd was founded by Tan Sri Dato’ Lim Kuang Sia with just an operating team of 5 people and has grown to a 28 billion pieces capacity giant. Kossan Bhd only started venturing into glove-making in 1988 when the AIDS pandemic was ravaging and demand for disposable gloves were seeing a strong uptick. Previously Kossan Bhd was in the business of manufacturing cutlass bearing used for in the fishing industry.

Kossan Bhd’s growth strategy is somewhat similar to its competitor Hartalega Holdings Berhad, where they put in the effort to build up their own plants instead of doing mergers and acquisitions.

Kossan Bhd’s main business is in the manufacturing of gloves, namely nitrile gloves, and rubber gloves. Gloves production accounts for around 88% of its total revenue. The remaining 12% is made up of contributions from technical rubber gloves and cleanroom products.

Last update: 20.11.2019

Dividends (5/5): ⭐ ⭐ ⭐ ⭐ ⭐

Value (3/5): ⭐ ⭐ ⭐

Financials (4/5): ⭐ ⭐ ⭐ ⭐

Growth (5/5): ⭐ ⭐ ⭐ ⭐

Business (3/5): ⭐ ⭐ ⭐

Reference: (i) MyKayaPlus Metrics Definition (ii) MyKayaPlus Metric Evaluation Scale

Management

Kossan Bhd was founded by Tan Sri Dato’ Lim Kuang Sia, who currently serves as the Chief Executive Officer (CEO). His brother Lim Leng Bung and son Lim Ooi Chow both serve as Executive Directors for Kossan Bhd. Messrs Lim Siau Tian and Lim Siau Hing are nephews of Tan Sri Dato’ Lim Kuang Sia and Lim Leng Bung who are also the Executive Directors of Kossan Bhd.

Tan Sri Dato’ Lim & family collectively hold around 55% of the ownership of Kossan Bhd, via direct and indirect interests. As of 2019, the total remuneration package of the total Kossan board of directors stands at around RM 19 million per annum, which is roughly 1% of their annual revenue.

Financial Performance

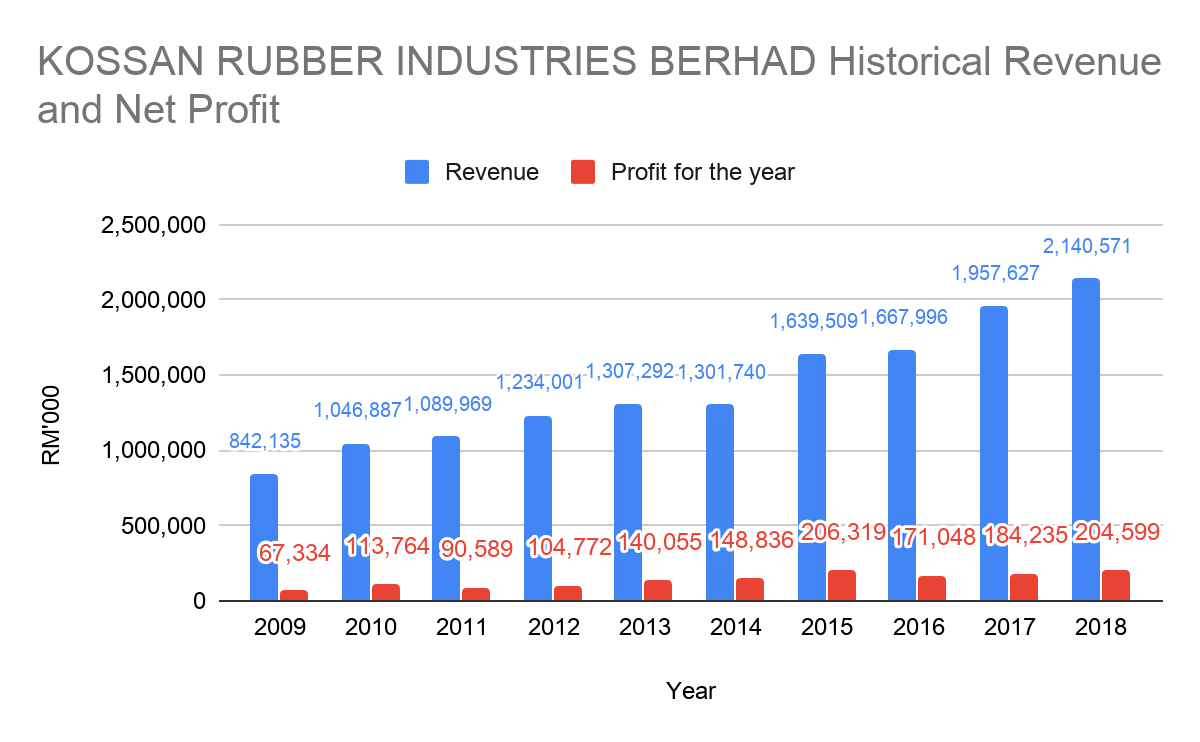

Kossan Bhd has seen great growth over the last 10 years. Net profit soared from RM 63 million to RM 205 million as of the year 2018. They have just commissioned their latest plant 17 to provide more capacity to tag on the double-digit growth forecast provided by the Malaysian Rubber Glove Manufacturers Association (MARGMA). Kossan Bhd plans to increase its capacity to 31 billion pieces of gloves by the year 2019.

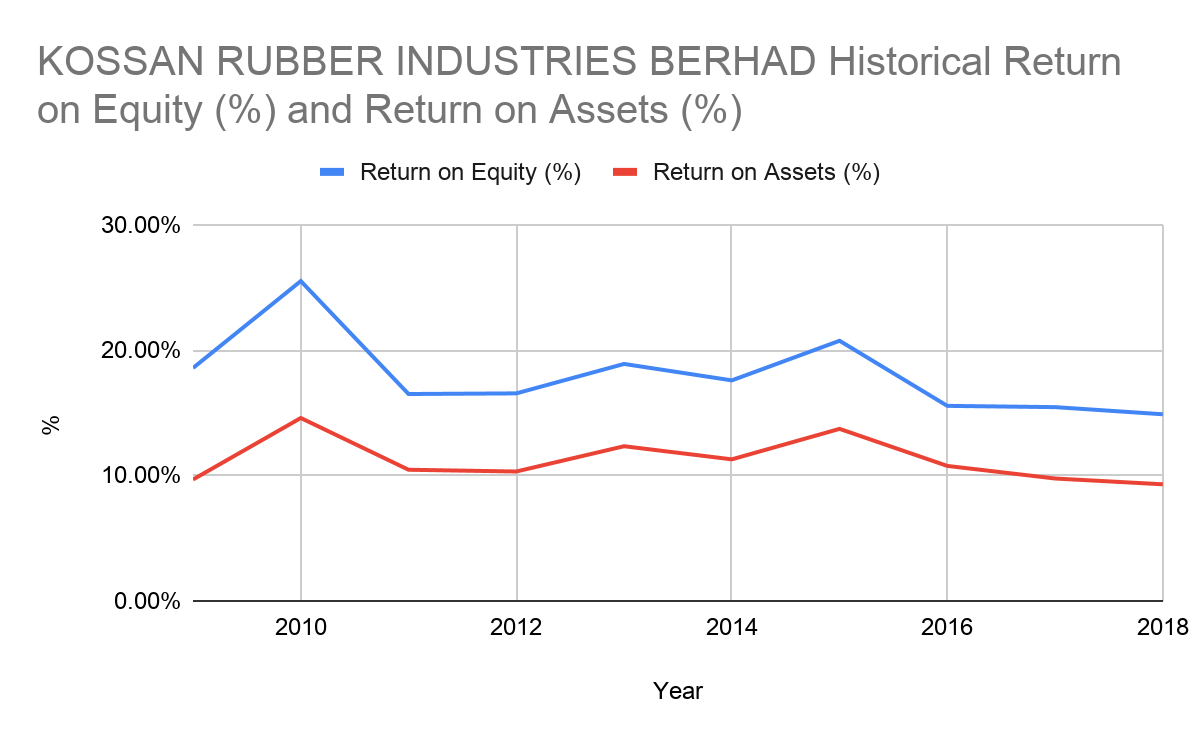

As of 2018, Kossan Bhd has a Return On Equity (ROE) of 15% and a Return Of Assets (ROA) of around 9%. Even though profit has increased quite a lot in the last 10 years, ROE and ROA are on a downtrend as the number of equity increases more than the profits generated. Kossan Bhd’s growth is skewed towards purchasing more land and setting up new factories to increase its productivity, hence the commissioning of new plants and additional lines usually consume more time compared to the merger and acquisition method.

Balance Sheet

| Year | Assets (RM’000) | Liabilities (RM’000) | Equities (RM’000) | Current Ratio |

| 2018 | 2,148,227 | 805,853 | 1,342,374 | 1.78 |

| 2017 | 1,865,064 | 686,793 | 1,178,271 | 1.99 |

| 2016 | 1,551,904 | 477,708 | 1,074,196 | 2.01 |

| 2015 | 1,476,295 | 499,849 | 976,446 | 2.14 |

| 2014 | 1,289,665 | 461,652 | 828,013 | 1.64 |

In the year 2019, Kossan Bhd has Assets of around RM 2.1 billion, liabilities of RM 806 million and equities of RM 1.3 billion. The current ratio is safely above 1, which is 1.78, which gives us assurance Kossan Bhd has enough current assets to meet its current liabilities.

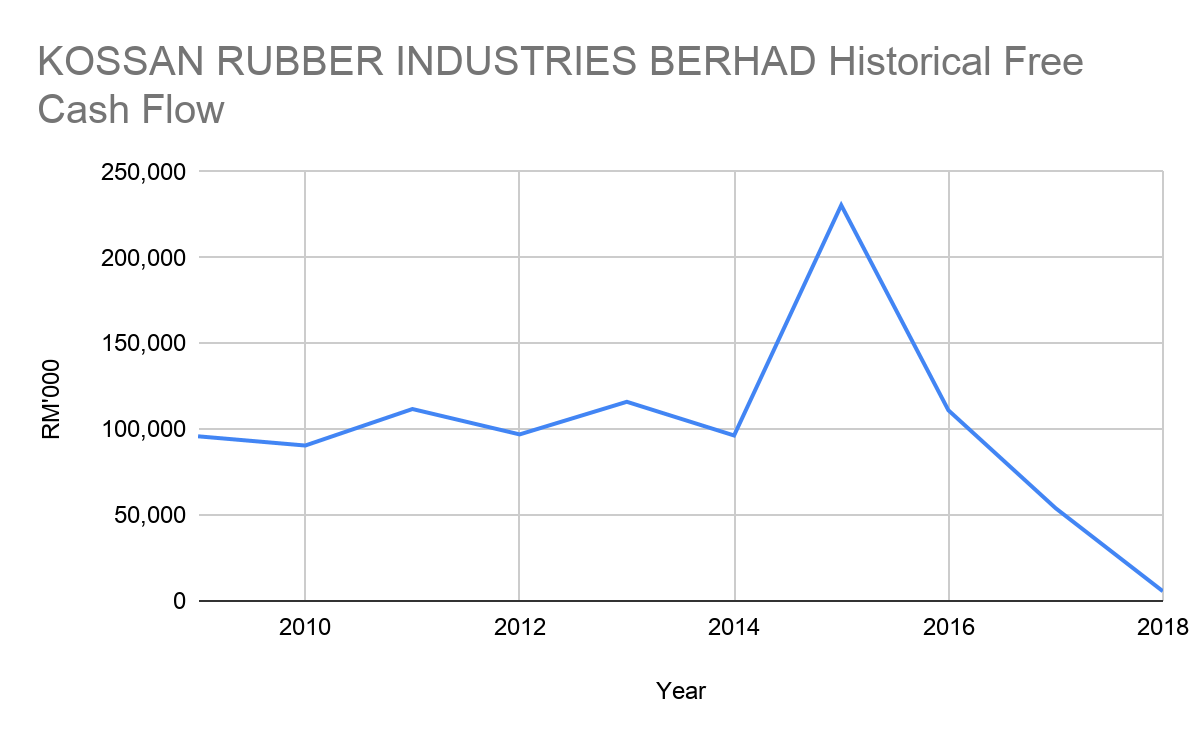

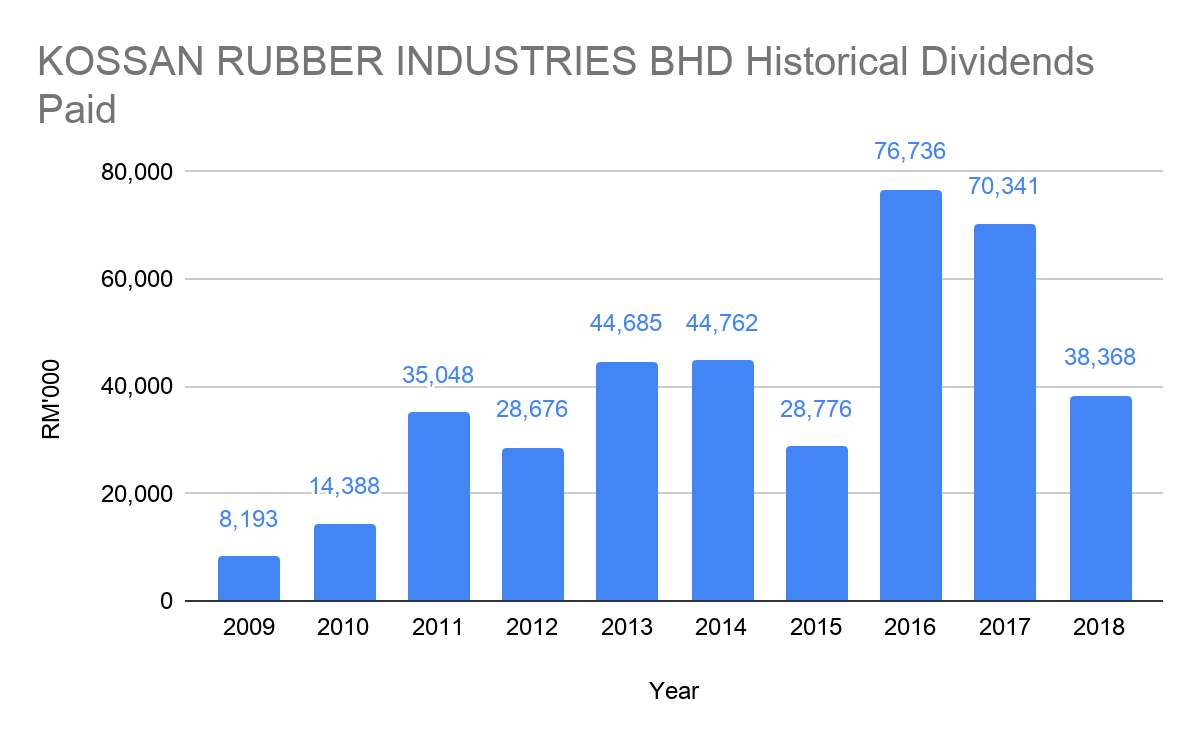

Free Cash Flow & Dividends Paid Out

Source: KOSSAN RUBBER INDUSTRIES BHD ANNUAL REPORT

It is evident that glove-making is not a profitable and cash-generating business. Kossan Bhd has seen its operating cash flow trending positively. However, there was a sharp dive as of the year 2018. During that year, the Group increased its capital expenditure with an aggregate cost of RM 317 million, particularly for plant 18 and plant 19 for increasing its capacity. So by taking off this one-off heavy capital expenditure, operating cash flow shows a significant uptick. Dividends paid has a 9 year compounded average growth rate of around 27% from 2009 till 2017. We purposely neglected the dividend paid out for 2018 because the company reserved its cash for its capital expenditure.

Like its other competitors, Kossan Bhd actually is considered a fantastic growth and dividend stock. They have shown a successful track record in increasing sales, profits, cash flow, and historical dividends paid out plus it is definitely trading at a cheaper price to earnings ratio compared to the big boys. Plus, Kossan Bhd also has a dividend policy of distributing a minimum of 30% of its annual profits to shareholders as dividends

Kossan Bhd is currently trading at a Price to Earnings ratio of roughly 24 times as of writing. Though it is relatively cheap compared to the 2 big boys in glove manufacturing, it’s trailing dividend yield is just at 1.45% per annum, which is not really attractive.

Price

MyKayaPlus Verdict

Kossan Bhd benefits as one of the key glove manufacturers and exporter of Malaysia, a country that dominates in the global market share scene at more than 50%. Coupled with the future forecast of global glove demands still at double-digit growth, it is no wonder all glove players including Kossan Bhd see a long term uptrend in share price and also earnings.

At a price to earnings ratio of around 24, investors are looking at a PE ratio the same as brewery companies which offer higher dividend yield and are more regulated.

But when it comes to sales growth, it is undeniable gloves demand will grow at a faster pace.

Do you see Kossan Bhd mounting a challenge to its 2 competitors? Let us know in the comments below!

Like our Kossan Bhd analysis? You would want to check out all the major glove players analysis

Top Glove Corporation Berhad analysis here

Hartalega Holdings Berhad analysis here

Supermax Corporation Berhad analysis here